The recent performance of gold has captured the attention of the mainstream media. We have even seen queues of people lining up at the ABC Bullion shop in Martin Place. So, for those investors who have gold, should you be selling? And for those that don’t yet have gold, is it too late?

Source: Creative Planning – Charlie Bilello

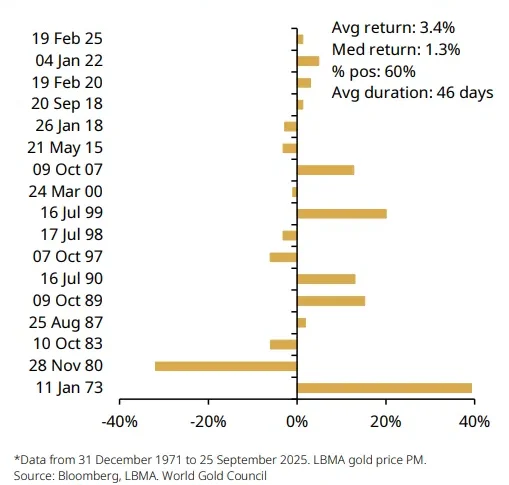

History has shown that when gold moves upward, it can move big

Let’s start with what is gold.

Gold is real money. Gold has been money and used as a store of wealth for over 5,000 years. Today, we live in a world where all currencies are fiat currencies, which means they are backed by absolutely nothing except the confidence in the issuing sovereign. It is my understanding that this is the first time in history (since 1971) that there has been no other currency anchored to something real like gold. Note that in the late 1790’s there was much political discussion about whether the US should adopt the gold standard or bimetallism (gold and silver) and was the determining factor for the Democratic Candidate, William Jennings Bryan, securing his party’s nomination.

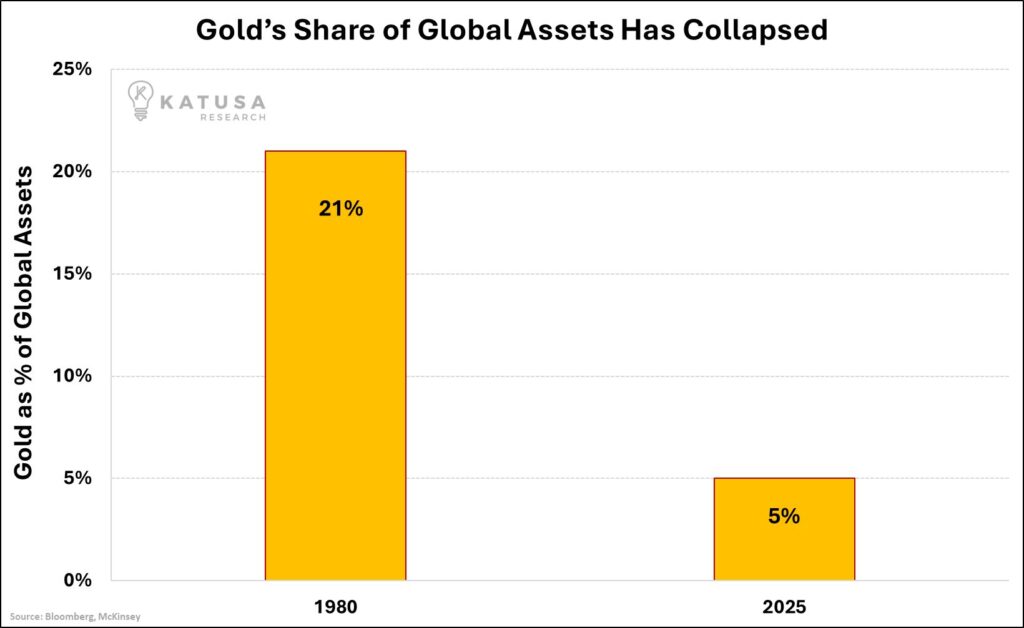

Since the closing of the gold window in 1971, the role of gold has been less dominant in the financial system by design.

Source: Katusa Research

As other parts of the financial system have become larger (through the issuing of cash and debt), the relative portion of gold has become less. This is an important point when we discuss what is a potential new “price” that is appropriate for gold.

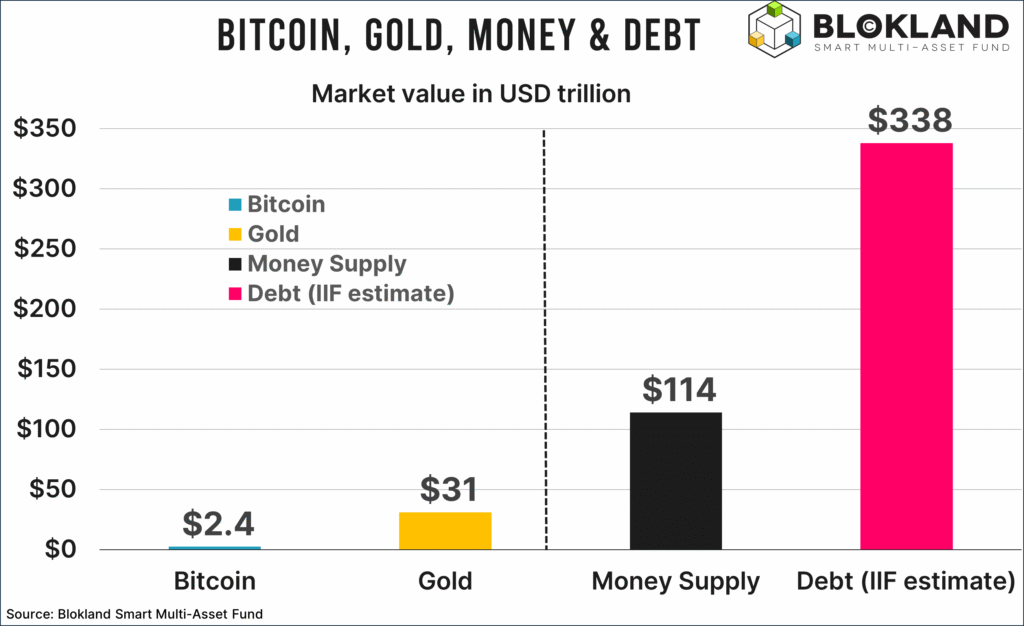

Source: Blokland Smart Multi-Asset Fund

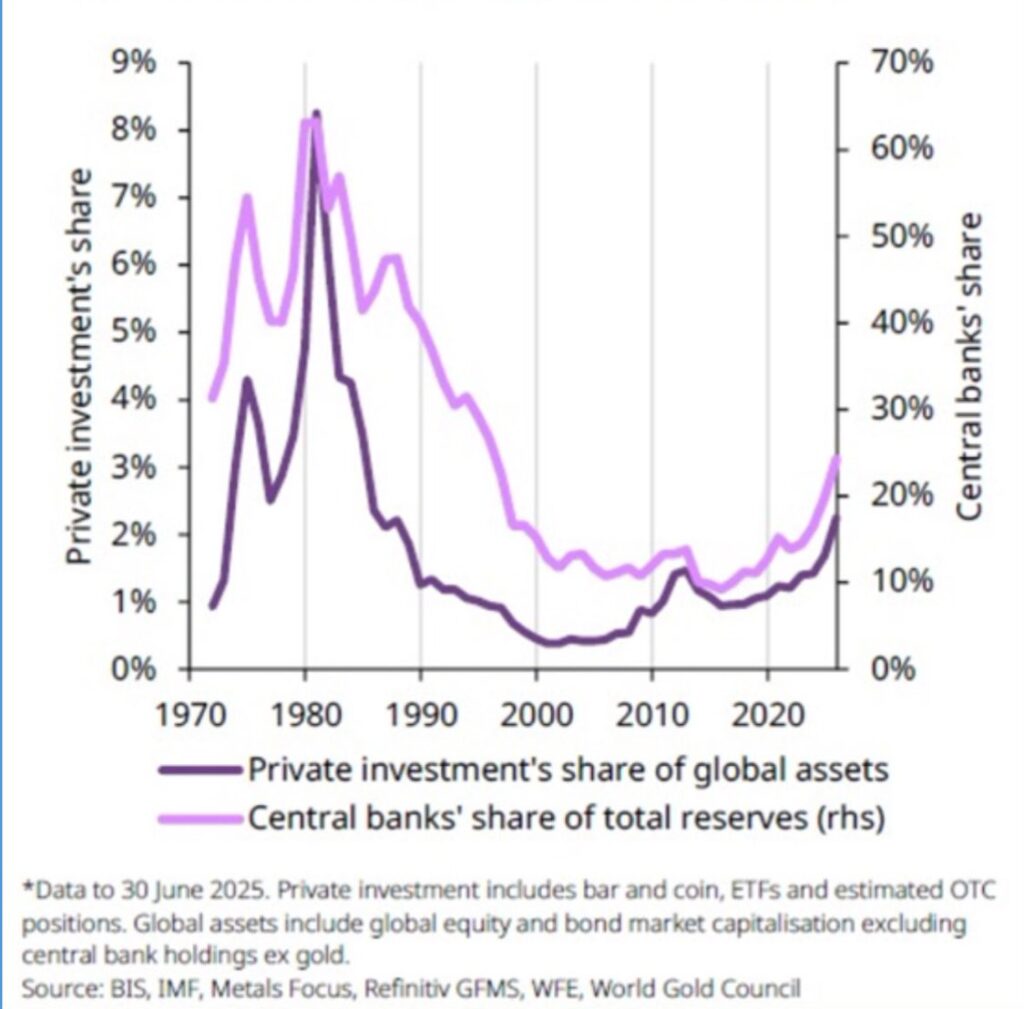

Therefore, it follows that the portion of wealth held by Central banks and Private investors in gold has decreased over the last 40 years. Again, this is an important point when we start thinking about what is a potential new “price” that is appropriate for gold.

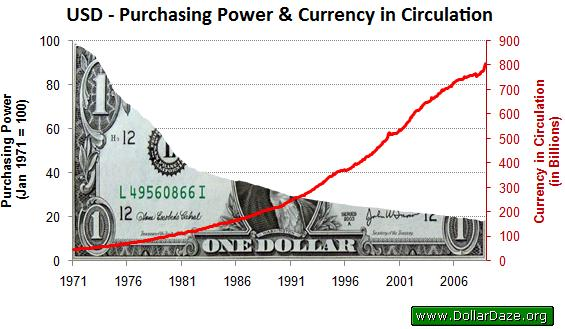

Before we move on, it is important to note that when I refer to the “price” of gold, this is measured in currency terms. By their very nature, fiat currencies devalue over time as measured by their purchasing power. This is often referred to colloquially as inflation. Note that the price of gold has risen in all currencies over time. Some more than others.

Source: www.DollarDaze.org

So why do we now own gold?

We own gold, in short, because it cannot be destroyed, replicated, and the supply is known to a reasonable degree of certainty. Furthermore, it exists outside the financial infrastructure and, in the words of JP Morgan, “Gold is money, everything else is credit”. By this, he means that gold is the only thing that does not have a counterparty. Any investment that has a counterparty, I will refer to generically as “the financial infrastructure”.

In short, we own gold as we are relying on the history associated with gold and the attributes above. In essence, many investors view this as an insurance policy to their other financial investments within the financial infrastructure, such as currency, bonds, property (by virtue that it is supported by loans and being easily taxed), and shares. If confidence in the financial infrastructure wanes, then gold becomes one of the few alternatives.

Gold has traditionally performed well in times that the share market has weakened as reflected by the chart below when the S&P500 has fallen 10% or more from all-time highs.

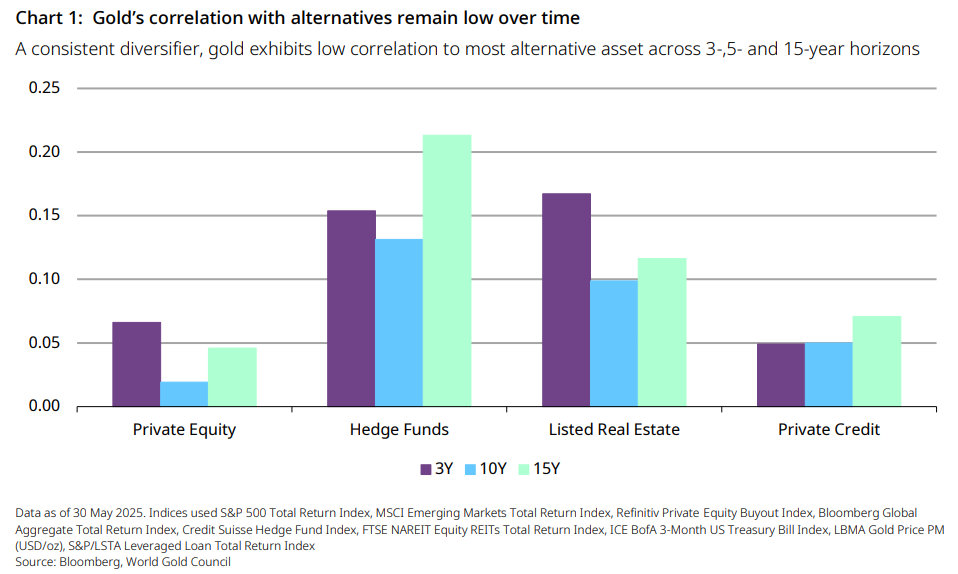

When we look at the correlation of gold relative to other assets from a portfolio management perspective, it makes sense to have an allocation to gold to help achieve risk-adjusted returns.

Source: Why smart investors are rebalancing alternatives with gold – LiveWireMarkets.com

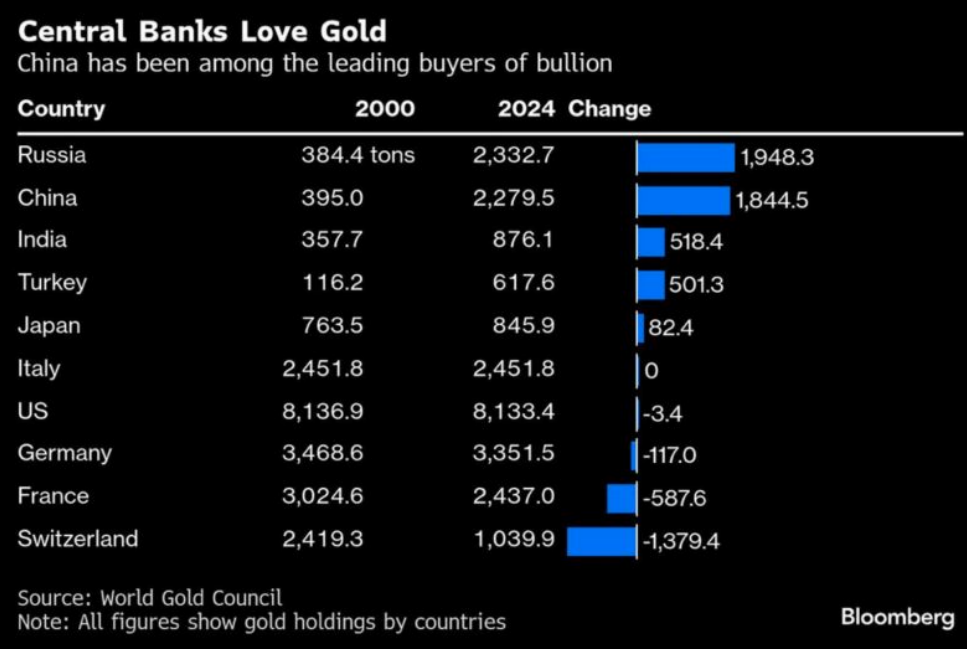

So, who owns gold? And who has recently been buying Gold?

Central banks have traditionally been big owners of gold. Keep in mind that previous monetary systems had the currency pegged to a level of gold that was stored in a vault at the Central Bank. Interestingly, the US Central Bank never sold any gold after coming off the Gold Standard in 1971. I think it is instructive to reflect on why they did not sell any of the gold. Note some other countries, most famously the UK, who sold at the bottom (referred to as “Brown’s Bottom” after the then Chancellor of the Exchequer, Gordon Brown), have sold gold throughout the years.

So who has been buying gold in the last few years? And why?

As you can see from the above table, China and Russia Central banks have been big buyers of gold.

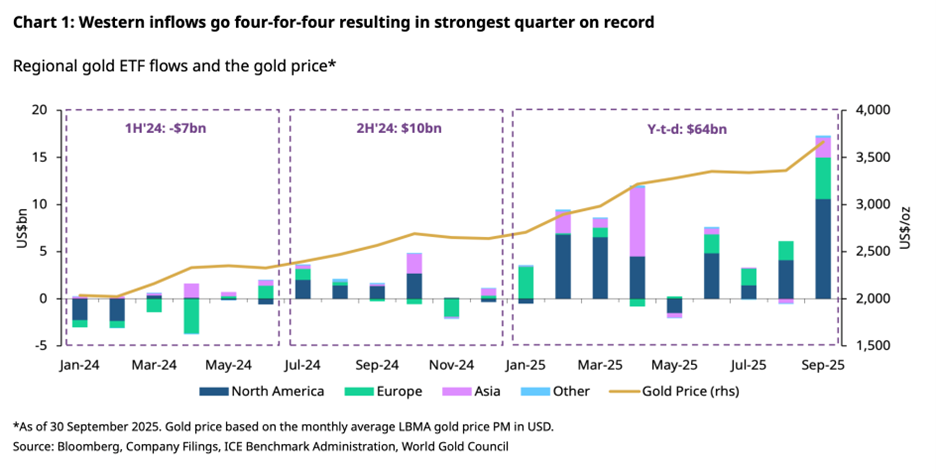

Interestingly, up until this year, the retail investor has not been even remotely interested in buying gold. This has now changed, as reflected by the amount of money flowing into ETFs below.

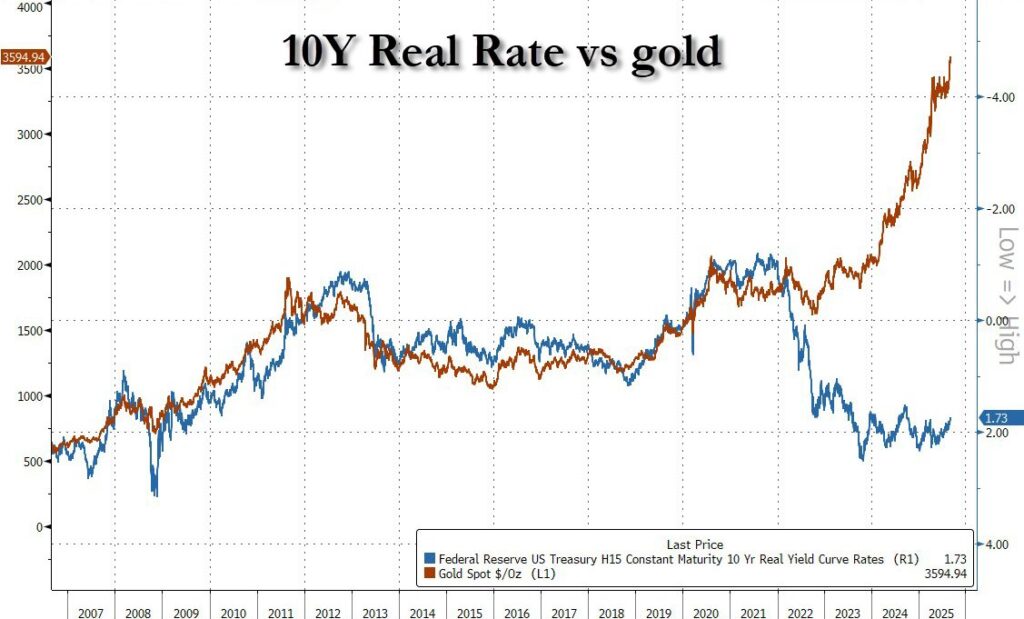

The other big change to the world over the last decade or so has been the weaponization of the USD and the destabilisation of the broader trading environment between the US and those countries that are not termed its allies. Russia had its USD reserves frozen in February 2022, which sent a very clear message to the world that if you get on the wrong side of the US, you will be isolated from the financial system. As a sovereign, this is a major risk and not something that countries like China and Russia were going to accept. Accordingly, we have recently seen a massive change in the correlation of the price of gold with the real (after inflation) level of interest rates. In my view, this is when the recent view of gold was fundamentally changed by the market.

China has been going around the world, chipping away at the need for it to trade with other countries in USD. As recently as a couple of weeks ago, BHP agreed to sell 30% of its iron ore to China in their own currency. Countries like Russia and other BRICS countries have increased trade dramatically with China in Yuan. These countries will receive Yuan for things such as the commodities they sell, and they can then use this currency to buy goods from China. After all, China is the factory of the world, so trade with these countries is a two-way street. If the country has leftover Yuan, they can then exchange it for gold, which acts as a neutral reserve asset that cannot be confiscated by another country (except for plundered as a result of war). Shanghai Gold Exchange has become the largest in the world, and China is setting up Gold exchanges all over the world for this purpose.

We have looked at the possibility of Countries having their currency and assets confiscated, but now let’s get back to the notion of confidence in the issuer of the fiat currency.

As shown by the graph earlier, the purchasing power of a fiat currency declines over time. As the famous Voltaire quote that fiat currency always returns to its intrinsic value… zero. This situation inevitably happens; it is just a matter of how much time it takes to get there.

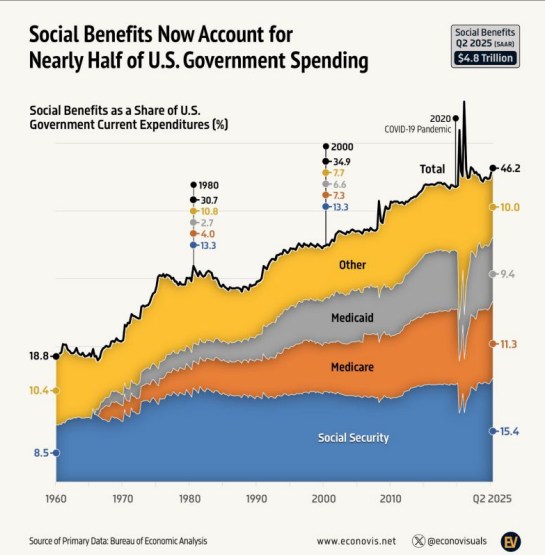

It is viewed by many, including myself, that the fiscal position in the US is now at a point where they will be forced to devalue their currency at an ever-increasing rate due to their fiscal position. The current US debt, not including unfunded liabilities such as Social Security, Medicare and pension plans, is USD $37 Trillion, and they are adding USD $2 Trillion to this each year. I have written previous blogs on the composition of how they spend these funds, and the fact is, they will find it very difficult (politically or socially) to claw back these expenditures. Note that social benefits now make up nearly 50% of government expenditure, before we include other non-negotiable expenses such as interest and defence spending.

Source: Econovis

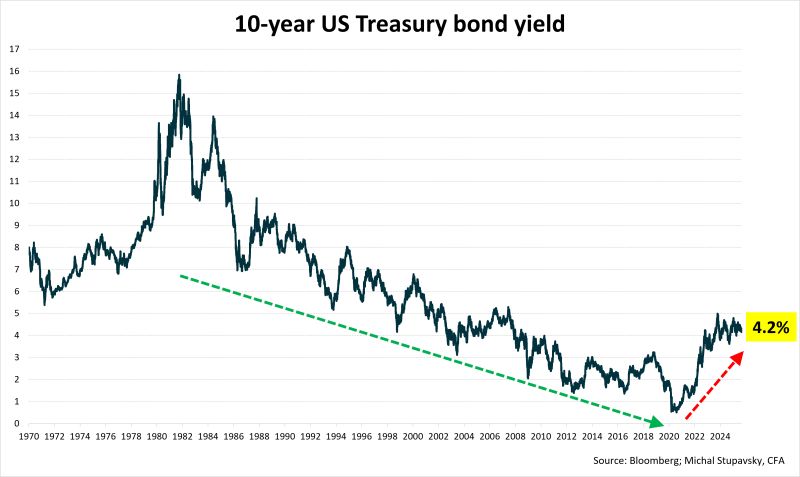

Furthermore, in a rising interest rate environment, the interest expense becomes higher at the same time the debt is increasing. In my opinion, this is why Donald Trump is putting a lot of pressure on Jerome Powell, Chairman of the Federal Reserve, to decrease interest rates. It’s not because the economy is altering; it is because the government cannot afford its debt, and by reducing rates, this may give them the option to term out the debt at lower interest rates.

Given the geopolitical situation, it would be wishful thinking to see any cut in defence spending, which is now approaching USD $1 Trillion. Quite the contrary, given the political will to reshore industry and gain control over supply chains, including access to commodities and resources, this can be seen as akin to putting the economy on a war footing. This will result in more debt and issuance of currency to be able to undertake these projects, which is highly inflationary.

The other consideration for the government budget would be the scenario of a recession. This would see the automatic stabilisers kick in, and the budget deficit would be even bigger, exacerbating the debt situation.

The other factor is that the US tax receipts are heavily reliant on the strength of the share market. Should there be a sell-off in the market because of, say, the failure of AI to deliver the expected returns, this would adversely impact upon tax receipts and ultimately the government debt.

All the above are positive for holding gold.

Should we be Selling Gold?

The first question I would pose is, will Central banks be sellers of gold?

I don’t think this will be the case for the reasons above. I would also say that many Western Central banks are behind the curve and have small gold reserves to what they should be holding relative to the size of their economies. Even Donald Trump recently posted the old adage “He who owns the gold makes the rules”. If these Western Central banks need to buy gold in bulk, what would this do for the gold price?

I had an exchange on social media with an economist recently who said that ‘gold was a bubble’ and ‘Central banks should sell their gold’. I simply asked what they would buy after they sold their gold, and he said they could just sit on the currency. I was shocked by his answer, but because of what I have laid out above, this will not happen in my opinion.

As discussed, gold has done well in periods of uncertainty. Given that the share market is looking at all-time high valuations, debt markets are quite large and with some recent high-profile defaults, will investors see these markets as “safer” options than gold?

As per the previous chart on the percentage of private ownership of gold as a portion of total assets is historically low. Based on the above reasoning on why you should own gold and the fact that there are few easible alternatives that look palatable at this juncture, I believe the view for gold over the next 3-5 years looks especially good. In saying this, there will be volatility, and if history is any guide, it will be severe volatility at times.

As the previous graphs showed, the current cash and debt markets globally comprise approx. USD $450 Trillion. If only 5% of this amount sought refuge in the gold market, which is only currently worth USD $30 trillion, this would have a substantial impact on the price of gold. This is not even allowing for any rotation of capital from the global property and share markets. It is also important to note that foreigners have a net position in the US of approximately USD $26 Trillion in USD assets (shares and bonds) at the moment. Should the USD weaken severely, there would be pressure on those foreigners to repatriate that capital.

Luke Gromen who is an analyst with Forest From The Trees and I thoroughly recommend that you subscribe to his services says that the fact that China and others are now using gold as a neutral reserve asset (after trade) the commodities markets which has flows 10-15 times the size of the gold market will also have a meaningful impact on the price of gold. In layman’s terms, the gold price will need to get higher to facilitate these transactions.

In my view, it appears the West is looking at Bitcoin as a possible alternative to gold, but the East is definitely looking at gold and not Bitcoin (they see it as a Western infrastructure). Given that the East have all the surpluses in trade and the advantage with purchasing Power Parity in making actual things in my mind, it is safer to go with what is their preference.

In short, you should seek professional financial advice on whether to hold gold and what portion of gold you should hold in your portfolio.

What will the future price of gold be?

In short, no one knows.

In saying that, the view within the investment world is changing.

Goldman Sachs and UBS, who are big players in the existing financial infrastructure, have recently put out price targets of USD $4,900 and USD $4,200 respectively.

People like Ray Dalio, who was the founder of Bridgewater Associates, have done a lot of education around the benefits of owning gold and have always said you should own 10% in a portfolio. Morgan Stanley and Jeffrey Gundlach, founder of DoubleLine Capital, have recently stated that an allocation to gold of 20% and 25% respectively is not excessive.

If we move back to a Gold Standard, the mathematics behind what the price of gold needs to be to facilitate is multiples higher than the current price. Even if we don’t have a formal gold standard, assuming the market determines by defacto that we should, the impact on price will be little different.

The other question is, if you sold your gold, what asset would you own in the hope of getting better returns than those of gold?

Personally, I have no idea what the future price of gold will be, but I do believe it will be higher than the current price if we were to look in 3 or 5 years’ time. Furthermore, from a portfolio perspective, it remains an important inclusion for most investors, notwithstanding recent moves.

This information is general advice and does not take account of investors’ objectives, financial situation or needs. Before acting on this general advice, investors should therefore consider the appropriateness of the advice having regard to their objectives, financial situation or needs.

Most investors understand the logic of the traditional 60/40 portfolio. Own a diversified mix of shares and bonds. Shares provide long-term growth. Bonds provide income…

We are currently in an investment environment that continues to evolve, where traditional models and assumptions are being challenged. Investors should now explore new ways…

I recently caught a podcast that featured Rick Rule being interviewed by Grant Williams, and thought the conversation was excellent and should be shared with…