Passive investing has grown enormously over the last 20 years.

The basic argument is easy to understand. Rather than trying to pick the best stocks, investors can buy an index fund or exchange-traded fund, keep costs low and get broad exposure to the market.

For many investors, this has worked well in an era of falling interest rates and rising share markets.

There has been much debate on the active and passive regards to price discovery and valuation, and the argument that if passive becomes so large, it becomes a self-fulfilling prophecy. However, there is a risk that is not discussed enough.

Passive investors do not simply own “the market”. They own whatever the index provider decides should be in the index.

That is an important difference.

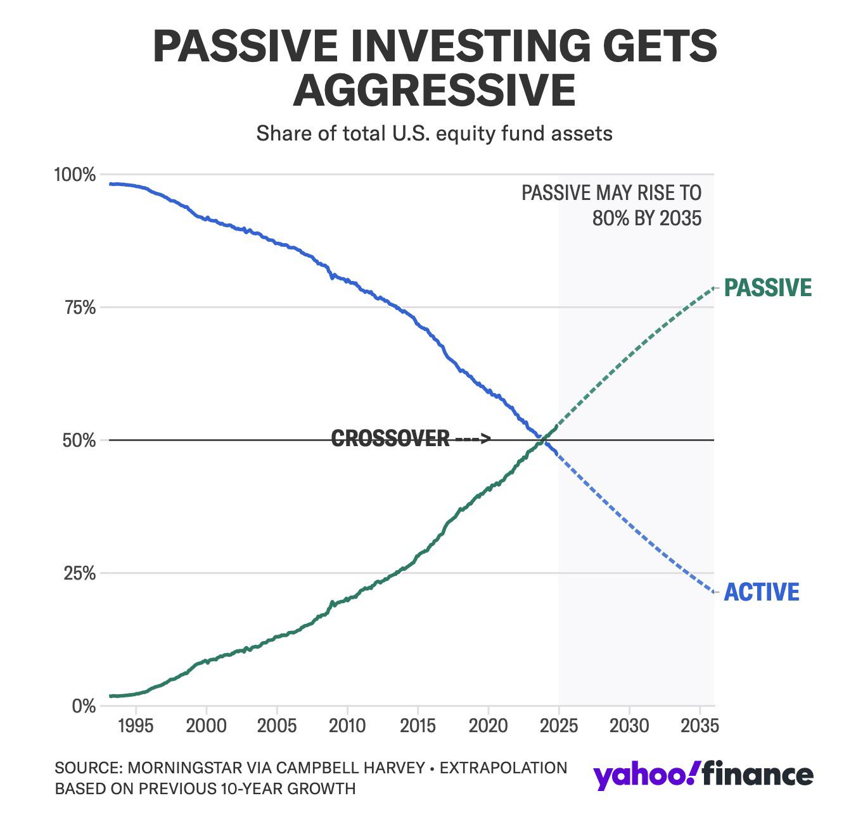

The chart shows passive investing moving from a small share of U.S. equity fund assets in the 1990s to around half today, with an extrapolation suggesting it could rise further over the next decade.

Why This Matters

This matters because passive investing is no longer a small part of the market.

It is now one of the dominant forces in equity markets; some believe this is a major risk for many unaware passive investors and an opportunity for more active participants.

As more capital moves into index funds and exchange-traded funds, index rules become more important. A change in index methodology can now influence where very large amounts of investor capital are allocated.

This is not just a technical issue. It affects retirement savings, superannuation funds, pension funds and ordinary investors who believe they are simply getting broad market exposure.

Most investors assume that if a company is included in a major index, it has already met a high standard.

They assume the company has been publicly listed for a reasonable period of time. They assume it has enough trading history. They assume there is enough liquidity. They assume the company has been tested by the public market before being included in the index.

Historically, these types of rules were important guardrails. They helped protect investors from being forced into newly listed companies before the market had properly assessed the business, the valuation and the risks.

Are we now seeing a weakening of these safeguards?

The Nasdaq-100 Rule Change

Nasdaq has changed the methodology for the Nasdaq-100 Index.

Under the new rules, a very large company that lists on Nasdaq may be able to enter the Nasdaq-100 after only 15 trading days, provided it is large enough. This is known as a “fast entry” rule.

The argument from Nasdaq is that some companies are now staying private for longer and are coming to market at a much larger size. Therefore, if a newly listed company is already one of the largest companies in the market, the index should be able to include it more quickly.

That argument has some merit. If a company is genuinely one of the largest listed businesses in the market, investors may expect a major index to reflect that.

However, there is another side to this. Fast index inclusion can turn passive investors into automatic buyers before there has been enough public market price discovery.

This is the concern.

Passive Buying Is Not Valuation Sensitive

An active investor can look at a company and decide whether the price makes sense.

They can ask:

- Is the valuation too high?

- Is the company profitable?

- Does the business model make sense?

- Is the balance sheet strong?

- Are the insiders aligned with ordinary shareholders?

- Is there enough liquidity?

A passive fund does not make that decision in the same way.

If the company is in the index, the fund buys it.

That is the mandate.

This means a company can receive large passive buying support simply because it qualifies for index inclusion. The buying is not necessarily based on valuation. It is based on index membership.

That creates a very different market dynamic, hence the potential risk or opportunity.

The SpaceX Example

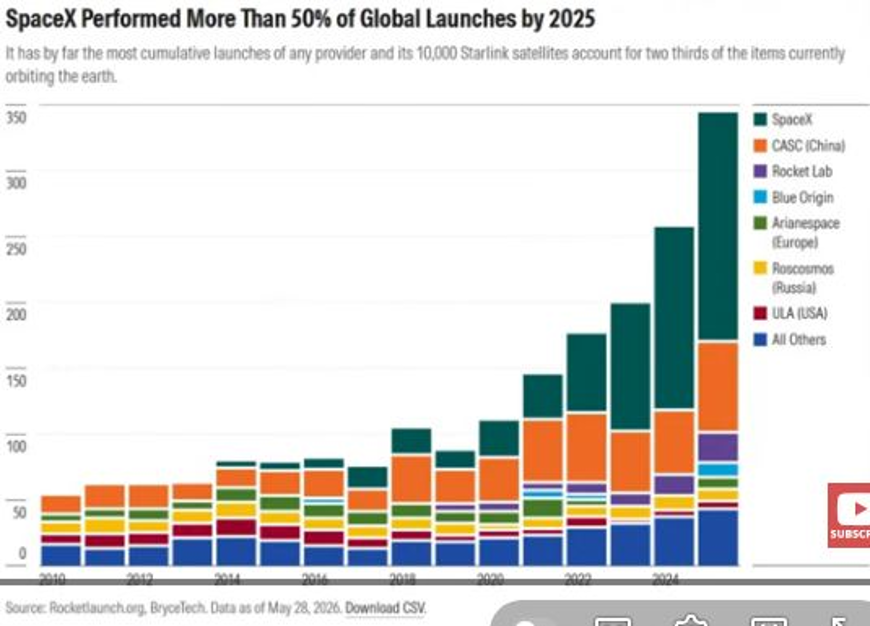

SpaceX is the obvious current example.

The chart below helps explain why SpaceX has attracted so much attention. It shows that by 2025, SpaceX accounted for more than 50% of global launches, reinforcing the point that this is a major business, even if the valuation debate remains separate.

This is not an argument that SpaceX is a poor business. It may be an exceptional business. It has real technology, real revenue and a major position in satellite communications and space launch services.

Morningstar has reportedly valued SpaceX at about US$780 billion, compared with an IPO target valuation of about US$1.75 trillion. In simple terms, an independent research house is saying the business may be worth less than half the proposed float valuation.

That valuation gap matters. For a smaller or less strategically important company, a proposed float at nearly double a credible independent valuation would normally be a major obstacle. Underwriters would need to justify the price, institutional investors would likely push back, and regulators or exchange reviewers would be expected to ask hard questions about disclosure, assumptions and investor protection.

The concern is that fast index inclusion and passive demand can soften that normal market discipline. If index funds become automatic buyers shortly after listing, the valuation risk is transferred to end investors who may not realise they are taking it.

The issue is not whether SpaceX is a good company. The issue is whether passive investors should be forced to buy a newly listed company shortly after it comes to market, before the public market has had time to properly assess the valuation.

A company can be a very good business and still be a poor investment at the wrong price. That point is often forgotten during periods of excitement; dare I say market tops.

If a company lists at a very high valuation and then quickly enters a major index, passive investors may be buying because the index requires them to buy, not because the valuation is attractive.

That is a very different proposition.

The AI IPO Pipeline

This issue may not stop with SpaceX.

The next potential test is the large AI companies, including OpenAI, the owner of ChatGPT, and Anthropic, the owner of Claude. These businesses are generating significant revenue, but revenue growth is not the same as durable profitability.

That distinction matters. Some AI companies are growing quickly, but they are also facing very high computing, data centre and infrastructure costs. The investment question is not simply whether people use the product. The question is whether the business can convert revenue into sustainable profits and cash flow at the valuation being sought.

This is not just a theoretical concern. Companies using AI are already starting to question whether the cost is justified. The transcript uses Uber as an example, noting that its AI token spending had become difficult to link directly to useful new consumer features. That is important because it shows the issue is not simply revenue growth for AI providers. The harder question is whether customers can or will keep paying for the product at scale, and whether that spending produces enough measurable value to support the valuations being discussed.

This is exactly the type of situation where traditional seasoning, liquidity and profitability requirements matter. A public market trading history gives investors time to assess the quality of revenue, the cost base, the margins and the governance structure before a company becomes a major index holding.

If large AI floats can achieve rapid index inclusion, passive investors may again become the natural buyer base before the market has had enough time to decide whether the business model is genuinely profitable, or simply large and fashionable.

The Float Issue

Another issue is the amount of stock actually available to the public. A company may have a very large total market value, but only a small percentage of its shares may be available for public trading.

If the public float is small, passive funds may all be trying to buy a limited pool of available shares. This can place upward pressure on the share price, particularly around index inclusion. The practical effect is that index inclusion itself can become a source of demand.

That can benefit early investors, founders and private shareholders. It may also support the share price in the short term. However, it does not remove the underlying investment risk for the passive investor.

The passive investor still owns the valuation risk.

Rules That Were Meant to Protect Investors

This is the key point.

Seasoning periods, liquidity requirements, profitability tests and float rules were not meaningless technical details.

They existed to protect market integrity.

They helped ensure that companies had a proper public trading history before being included in major indices.

They helped ensure that index funds were buying companies that had been tested by public markets.

They helped reduce the risk that retirement savings and long-term investment capital would be forced into companies too early.

When these rules are loosened, the balance of power can shift.

It can shift away from the ordinary investor and toward the company coming to market or more instructive to the people or insiders behind the company coming to the market.

I am not saying every company using the new rules is poor quality, just that the investor protection framework has changed.

The Penalty Problem

This is where the issue becomes more uncomfortable.

If an insider, founder or early investor misleads the market, trades on undisclosed information or manipulates a security, the existing securities laws still apply. In the United States, Rule 10b-5 prohibits material misstatements, omissions and fraudulent or deceptive conduct in connection with buying or selling securities. That is not the concern here.

The concern is more subtle. If the rules themselves allow a company to list at an aggressive valuation, enter an index quickly, maintain a limited public float and create forced passive demand, the behaviour may not be punished in the way investors might expect. It may be fully disclosed. It may comply with the revised methodology. It may be accepted by underwriters and the exchange.

Under the previous framework, seasoning, liquidity and profitability requirements acted as practical discipline. They made it harder for insiders to transfer valuation risk to passive investors before the company had been tested by public markets.

Under the revised framework, some of that discipline is removed. The potential penalty shifts away from the people structuring the float and toward the end investor, who may simply pay too high a price through an index fund or exchange-traded fund.

This is the distinction investors need to understand. The issue may not be clear-cut illegality. The issue may be legal exploitation of the rules. If the structure is permitted, the financial consequence may fall mainly on passive investors rather than on the issuers or early shareholders who benefited from the structure.

What This Means for Investors

Low-cost index investing can still be useful. It can provide broad market exposure and it can be difficult for many active managers to outperform after fees. Passive investing is just one of the tools available to investors.

However, investors need to understand what they own. An index is not a perfect representation of economic reality. It is a rules-based product.

Those rules can and have recently changed.

When they do, passive investors are carried along automatically.

That creates risks that are not always obvious, including:

- concentration risk;

- valuation risk;

- governance risk;

- liquidity risk;

- methodology risk; and

- forced buying risk.

The more money that tracks an index, the more powerful the index rules become.

Inclusion creates demand. Exclusion removes demand.

This is no longer just a technical issue. It is a major capital allocation issue.

The Takeaway

Passive investing is not as passive as many investors think.

The investor may be passive, but the index rules are active.

Someone is deciding which companies are included, how quickly they are included and how much weight they receive. When those decisions change, investors are exposed whether they realise it or not.

For long-term investors, the key message is simple.

Do not assume that an index fund removes the need to understand risk. There is always risk with investing, and as an investor, you need to be aware of them and manage them accordingly.

Passive investing may reduce stock selection risk, but it does not remove valuation risk, liquidity risk or concentration risk. Most importantly, it does not remove index construction risk.

In my view, this reinforces the need to look through portfolios and understand what is actually owned, rather than relying on labels such as “passive”, “index” or “diversified”. Passive investing is just a tool available to investors, and you need to know how that tool can be used effectively.

This information is general advice and does not take account of investors’ objectives, financial situation or needs. Before acting on this general advice, investors should therefore consider the appropriateness of the advice having regard to their objectives, financial situation or needs.

Written by Rob Coyte

CEO – Shartru Wealth